The Wisdom of the Few: Skilled Traders and Prediction Market Accuracy

with Gloria Heesen

Working paper · Present at CFE 2026 (Vietnam) (scheduled)

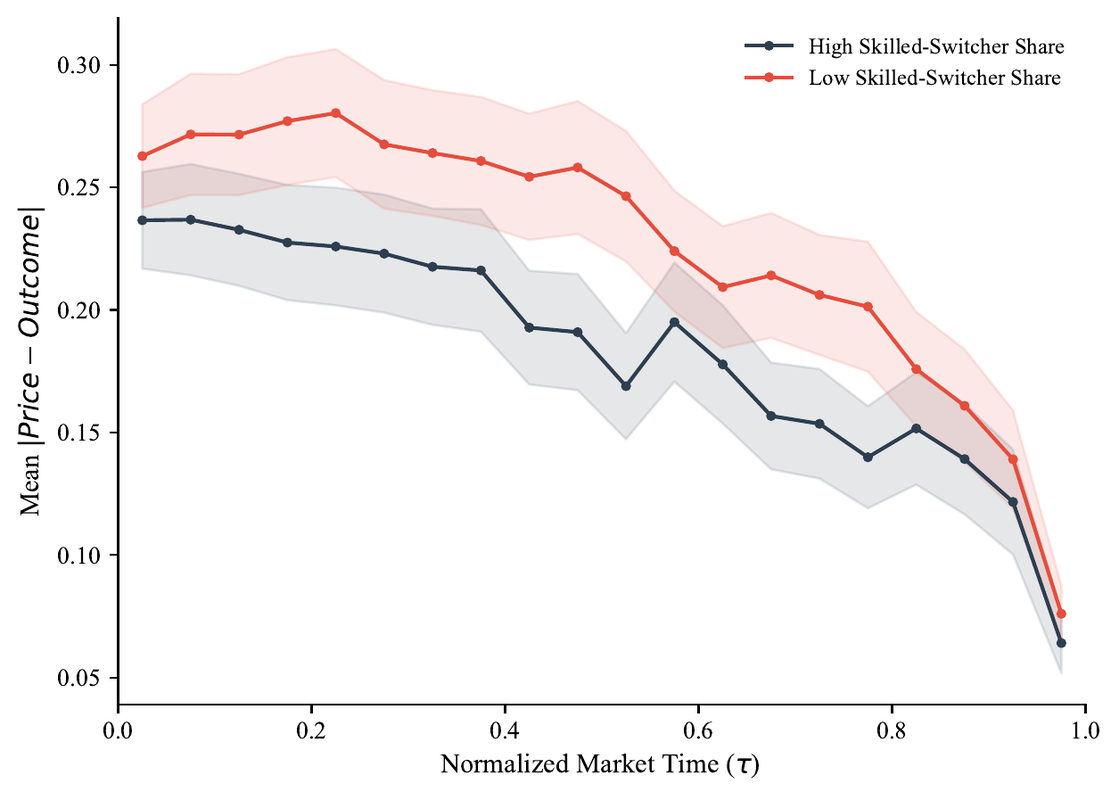

We study how participant composition affects pricing accuracy in prediction markets using transaction-level data from Polymarket. We classify participants by execution behavior across markets: makers, who post liquidity and bear adverse selection costs; takers, who cross the spread; and switchers, who do both. A model where signal-holders choose their execution role rationalizes cross-market role-mixing as a behavioral signature of private information. Most switchers are indistinguishable from takers. A small subset, identified by a skill screen, drives the result: a one-standard-deviation increase in their volume share is associated with 19% lower pricing error at close. A Brier decomposition attributes the effect to price calibration, not to how well markets distinguish outcomes. These skilled switchers carry permanent price impact and earn improving returns with experience. Takers persist despite losses. Market accuracy traces to a thin layer of informed participants.